Career Pilot: Pulse Check

Things are booming in pilot hiring, but Will it last?

Each March, the FAA convenes industry leaders, prognosticators, and planners to gaze into a crystal ball to see where the industry is headed. The FAA Aerospace Forecast Fiscal Years 2017-2037 is the government’s assessment in 89 pages of charts, graphs, and narratives. A high-level look at the major and regional airlines as well as general aviation is a manageable exercise, although admittedly a less-than-exciting task. Yet, remember that aviation is a transportation business and a look at your future through an accountant’s eye is prudent.

Each March, the FAA convenes industry leaders, prognosticators, and planners to gaze into a crystal ball to see where the industry is headed. The FAA Aerospace Forecast Fiscal Years 2017-2037 is the government’s assessment in 89 pages of charts, graphs, and narratives. A high-level look at the major and regional airlines as well as general aviation is a manageable exercise, although admittedly a less-than-exciting task. Yet, remember that aviation is a transportation business and a look at your future through an accountant’s eye is prudent.

Major airlines. The recession of 2007 to 2009 marked a fundamental change in the operations and finances of U.S. airlines. Air carriers fine-tuned their business models to minimize losses by lowering operating costs; eliminating unprofitable routes; and grounding older, less fuel-efficient aircraft. To increase operating revenues, carriers initiated new services customers were willing to purchase and started charging separately for services that were historically bundled in the price of a ticket (for example, baggage fees).

Major airlines. The recession of 2007 to 2009 marked a fundamental change in the operations and finances of U.S. airlines. Air carriers fine-tuned their business models to minimize losses by lowering operating costs; eliminating unprofitable routes; and grounding older, less fuel-efficient aircraft. To increase operating revenues, carriers initiated new services customers were willing to purchase and started charging separately for services that were historically bundled in the price of a ticket (for example, baggage fees).

The industry experienced an unprecedented period of consolidation with four major mergers in five years. These changes, along with capacity discipline exhibited by carriers, resulted in a seventh consecutive year of profitability for the industry in 2016.

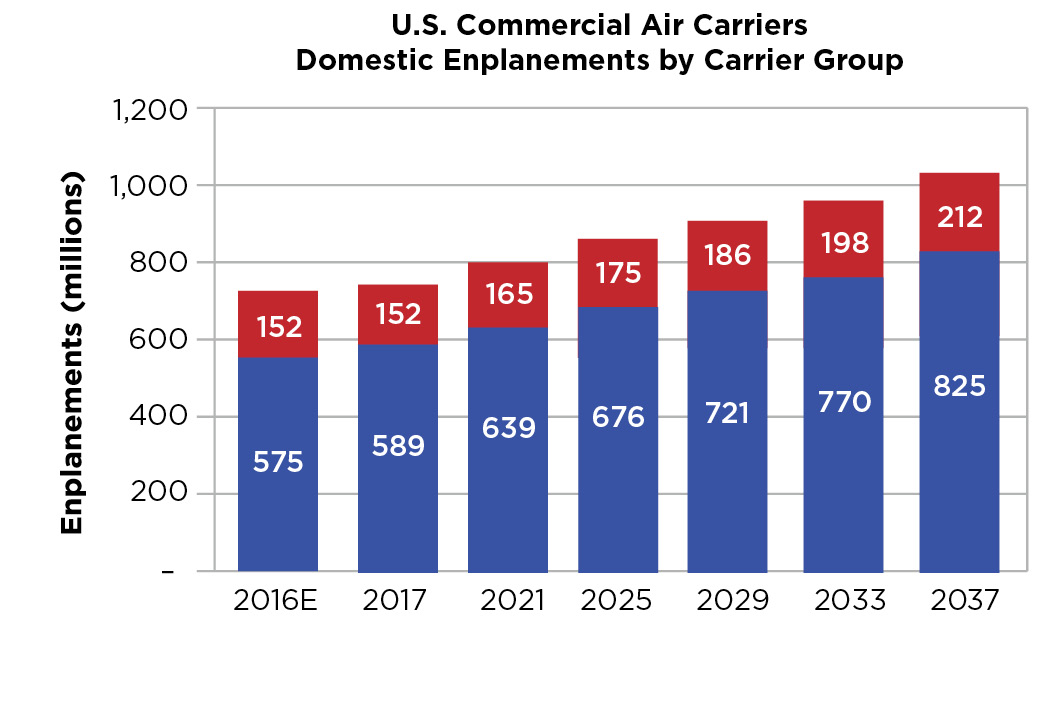

Looking ahead there is optimism that the industry has been transformed from that of a boom-to-bust cycle to one of sustainable profits. The forecast calls for U.S. carrier passenger growth in the next 20 years to average 1.9 percent per year, slightly slower than 2016’s forecast.

Looking ahead there is optimism that the industry has been transformed from that of a boom-to-bust cycle to one of sustainable profits. The forecast calls for U.S. carrier passenger growth in the next 20 years to average 1.9 percent per year, slightly slower than 2016’s forecast.

Regional airlines. The regional market has continued to shrink as the regionals compete for even fewer contracts with the remaining dominant carriers; this has meant slow growth in enplanements and yields. The regionals have less leverage with the mainline carriers than they have had in the past as the mainline carriers have negotiated contracts more favorable for their bottom lines. Furthermore, the regional airlines are facing large pilot shortages and tighter regulations regarding pilot training. Regional airline capital costs have increased in the short term as they continue to replace 50-seat regional jets with more fuel-efficient 70-seat jets. This move to the larger aircraft will prove beneficial in the future, however, since their unit costs are lower. The big picture shows future growth which, of course, means more aircraft and a need for more pilots to fly them.

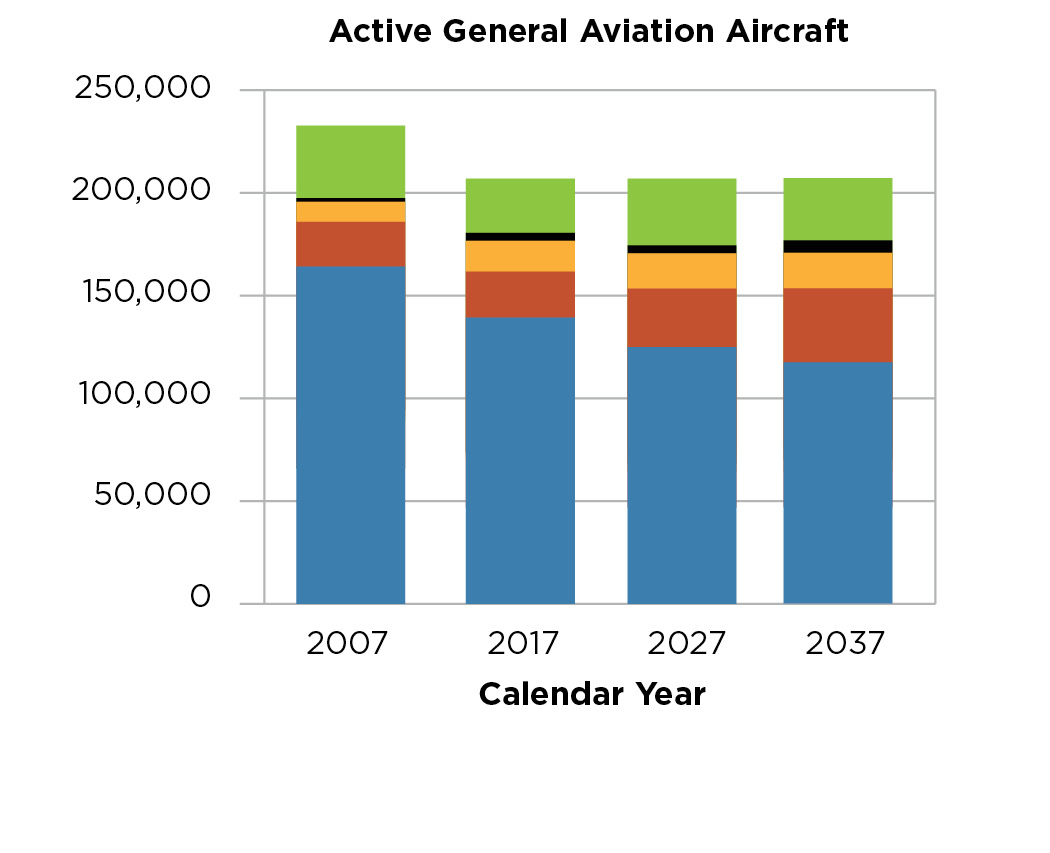

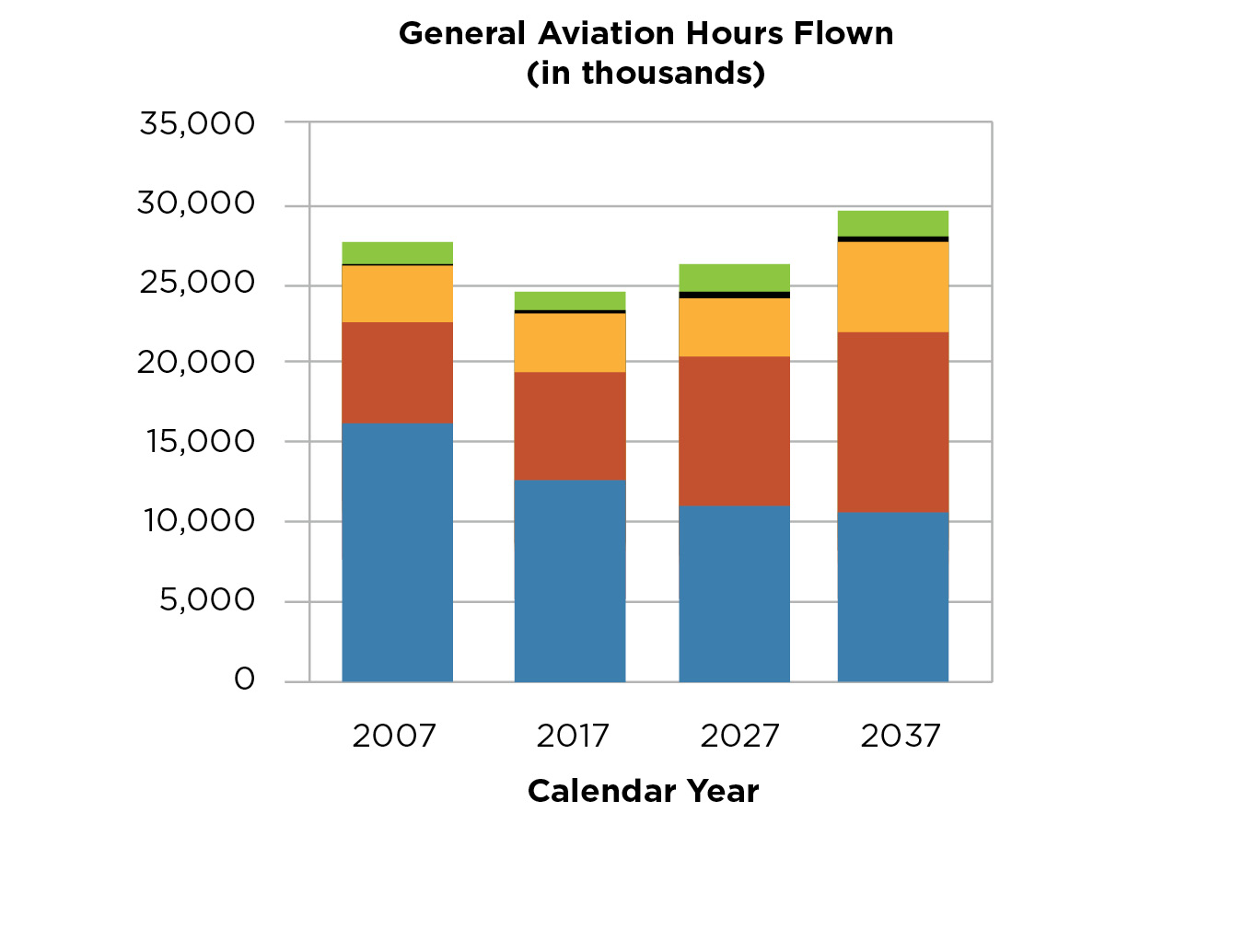

General aviation. Nothing is more telling about the state of general aviation than projected fleet size, hours flown, and the number of pilots.

General aviation. Nothing is more telling about the state of general aviation than projected fleet size, hours flown, and the number of pilots.

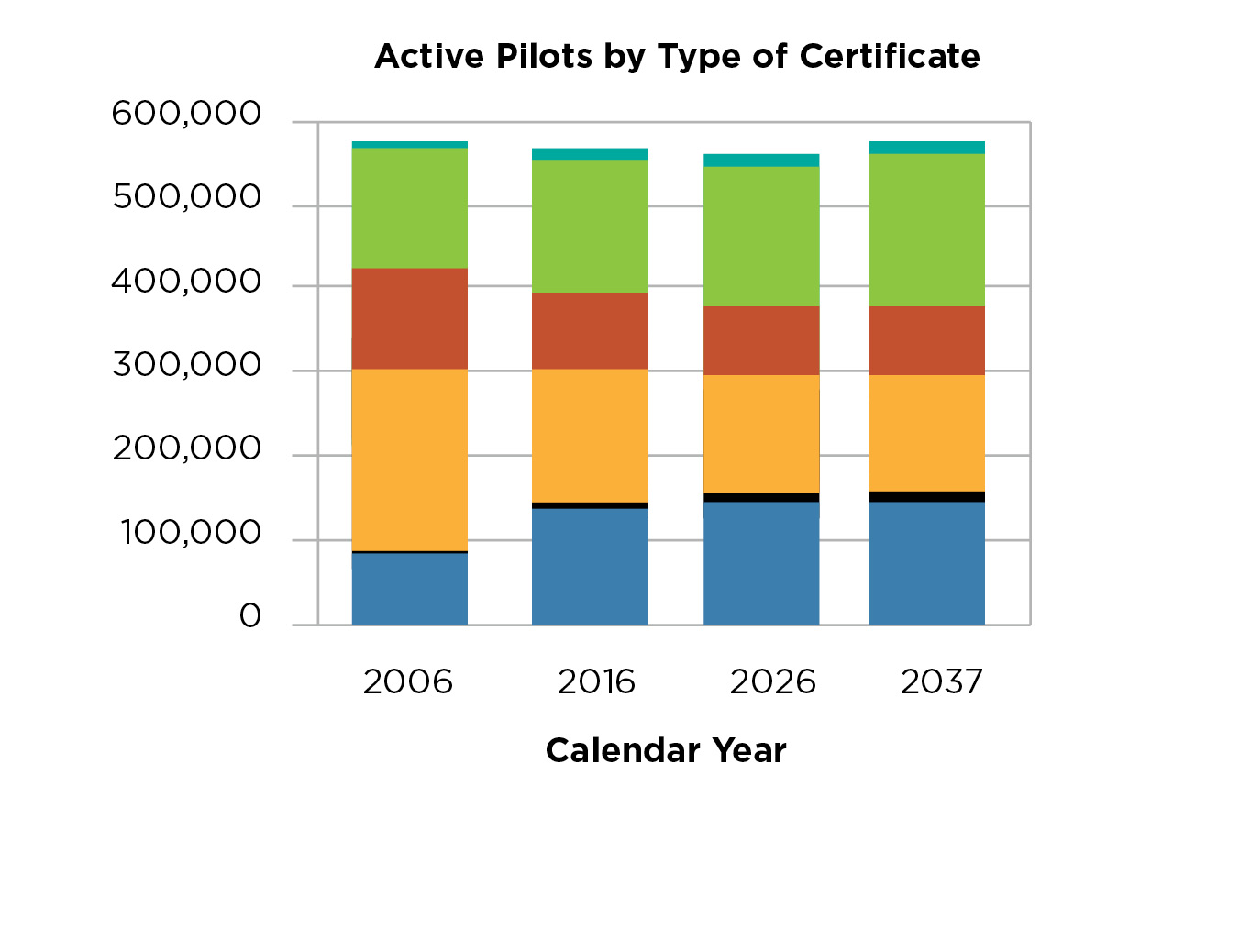

The FAA conducts a forecast of pilots by certification categories, using the data compiled by the administration’s Mike Monroney Aeronautical Center. There were 584,362 active pilots certificated by the FAA at the end of 2016. Although private and commercial pilot categories continued their declining trends, airline transport pilot and student pilot certificates continued to increase. Since 2011, the student pilot numbers have been rising and reached 128,501 in 2016.

You can take some comfort in knowing that the future looks reasonably bright for anyone who has cast his or her fate with the aviation industry.

Related Articles